For sophisticated aircraft owners, a private jet is more than a transportation asset. It is a strategic financial instrument capable of generating significant tax advantages when structured correctly. While many buyers focus on acquisition price, operating costs, and aircraft capabilities, experienced investors often evaluate a transaction through an entirely different lens: after-tax return on investment.

Understanding private jet depreciation can dramatically alter the economics of aircraft ownership. In many situations, depreciation schedules, bonus depreciation opportunities, and strategic ownership structures can reduce tax liabilities while improving cash flow. However, achieving these advantages requires careful planning, compliance, and expert guidance.

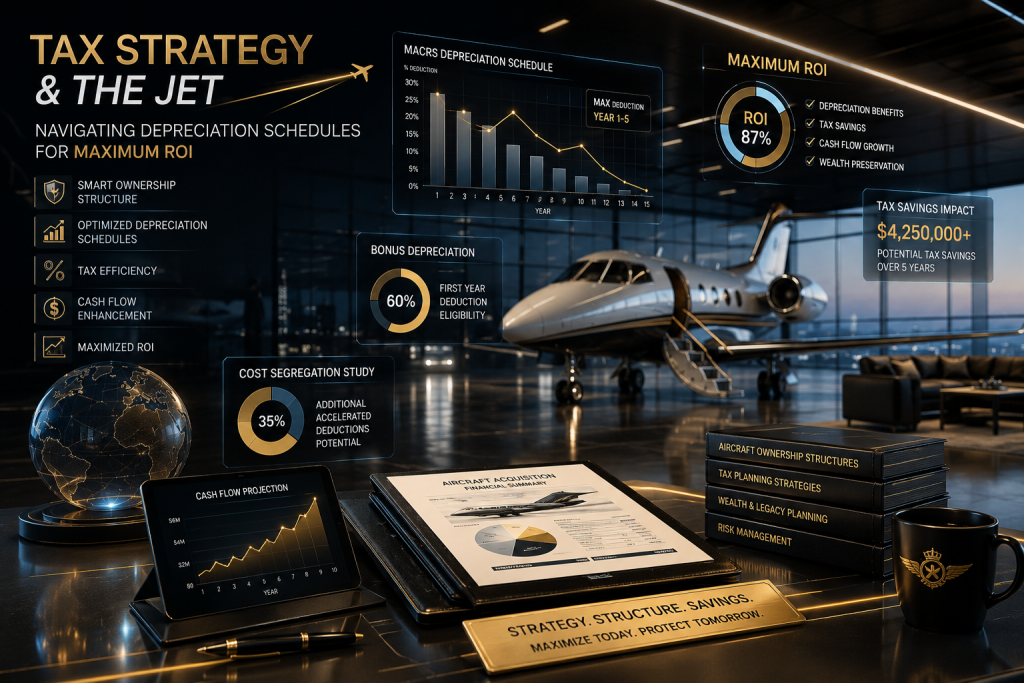

The difference between a well-structured acquisition and a poorly planned one can amount to millions of dollars over the life of an aircraft.

This guide explores how high-net-worth individuals, family offices, corporations, and aviation operators navigate depreciation schedules to maximize ROI while minimizing risk.

By: PrivateJetio Aviation Advisory Team

Why Tax Strategy Matters in Aircraft Ownership

Private aviation occupies a unique position within the tax landscape.

Unlike luxury assets such as yachts, exotic vehicles, or vacation properties, aircraft frequently serve legitimate business purposes. When an aircraft qualifies as a business asset, owners may be able to claim depreciation deductions that reduce taxable income.

The financial impact can be substantial.

Consider a corporation purchasing a $20 million aircraft used primarily for business operations. Depending on applicable regulations, utilization patterns, and ownership structure, a significant portion of that asset’s value may become deductible over time.

This transforms aircraft ownership from a simple capital expenditure into a sophisticated financial planning exercise.

The most successful aircraft buyers rarely ask:

“How much does this jet cost?”

Instead, they ask:

“What is the net after-tax cost of ownership?”

That distinction separates transactional buyers from strategic buyers.

Understanding Private Jet Depreciation

At its core, depreciation recognizes that assets lose value over time.

Governments allow businesses to deduct portions of an asset’s cost throughout its useful life rather than requiring the entire purchase cost to remain on the balance sheet indefinitely.

Aircraft are no exception.

When a qualifying aircraft is used for business purposes, owners may be entitled to claim depreciation deductions under applicable tax regulations.

These deductions effectively spread the cost of the aircraft over a designated period.

The result is a reduction in taxable income.

Why Depreciation Matters

Depreciation creates three major advantages:

- Reduction of taxable income

- Improved cash flow management

- Enhanced investment returns

A properly structured depreciation strategy can significantly improve the economics of ownership without changing the aircraft itself.

The aircraft performs the same missions.

The difference lies entirely in financial structuring.

The Evolution of Aircraft Tax Planning

Over the past two decades, governments have periodically introduced incentives designed to stimulate business investment.

Aircraft have frequently qualified for these incentives when used for legitimate business purposes.

As a result, sophisticated buyers often accelerate acquisition timelines to take advantage of favorable tax treatment.

This is why many aircraft transactions occur near fiscal year-end.

The timing of delivery can materially impact tax outcomes.

An aircraft delivered days before year-end may produce vastly different financial results compared to one delivered weeks later.

This is one reason elite buyers integrate tax advisors into the acquisition process from the earliest stages.

Tax planning should never occur after the transaction closes.

It should influence the transaction itself.

Bonus Depreciation and Its Strategic Impact

Among the most significant developments in recent years has been the use of bonus depreciation.

Bonus depreciation allows qualifying businesses to deduct a substantial portion of an eligible asset’s cost in the year it is placed into service.

For aircraft buyers, the implications can be extraordinary.

Rather than spreading deductions across many years, owners may be able to accelerate deductions and realize immediate tax benefits.

Why Sophisticated Buyers Pay Attention

Accelerated depreciation can:

- Improve liquidity

- Reduce near-term tax obligations

- Increase available investment capital

- Improve aircraft ROI calculations

For entrepreneurs, private equity principals, and business owners experiencing unusually profitable years, accelerated deductions may provide particularly valuable tax planning opportunities.

However, qualification requirements are complex.

Aircraft usage, ownership structures, documentation standards, and operational compliance all influence eligibility.

Failure to meet these standards can lead to audits, penalties, and recapture issues.

This is why experienced aviation advisors coordinate closely with tax attorneys and accountants throughout the acquisition process.

The Role of the MACRS Depreciation Schedule

One of the most important frameworks in U.S. aircraft taxation is the MACRS depreciation schedule.

Modified Accelerated Cost Recovery System (MACRS) establishes recovery periods and depreciation methodologies for qualifying business assets.

Aircraft frequently fall within specific recovery classifications depending on usage patterns and operational characteristics.

Understanding Recovery Periods

Recovery periods determine how quickly deductions can be claimed.

The shorter the recovery period:

- The faster deductions occur

- The greater near-term tax benefits become

- The stronger cash-flow advantages may be

However, maximizing speed is not always the optimal solution.

Sophisticated tax planning balances:

- Current tax savings

- Future tax positions

- Investment objectives

- Long-term ownership plans

A depreciation strategy should support broader financial goals rather than simply generating the largest immediate deduction.

Aircraft Ownership Structure and Tax Efficiency

The structure through which an aircraft is owned can significantly influence tax outcomes.

Many buyers focus exclusively on selecting the aircraft itself while neglecting ownership architecture.

This can be a costly mistake.

An effective aircraft ownership structure considers:

Individual Ownership

Direct ownership may offer simplicity but can introduce liability, tax, and operational limitations.

Corporate Ownership

Many organizations hold aircraft through operating companies or dedicated aviation entities.

This structure may improve administrative efficiency and compliance management.

Holding Companies

Certain owners establish dedicated entities specifically designed to own aviation assets.

This approach can create operational separation and support broader wealth management objectives.

Family Office Structures

Ultra-high-net-worth families frequently integrate aircraft ownership into larger wealth preservation frameworks.

Aircraft become one component of a coordinated investment and asset management strategy.

The optimal structure depends on:

- Jurisdiction

- Tax profile

- Business activities

- Flight usage

- Estate planning objectives

- Asset protection goals

There is no universal solution.

Each aircraft acquisition deserves independent analysis.

Business Aviation Tax Benefits Beyond Depreciation

Depreciation often receives the most attention, but it is only one element of a larger strategy.

Experienced aircraft owners evaluate the complete spectrum of business aviation tax benefits.

Potential considerations may include:

- Operating expense deductions

- Interest expense treatment

- State tax planning

- Sales and use tax strategies

- Lease structures

- International ownership considerations

- Cross-border operational planning

Viewed collectively, these elements can materially influence ownership economics.

This broader perspective explains why leading family offices and corporations rarely approach aircraft acquisition as a simple purchase.

Instead, they view it as a strategic capital allocation decision.

Private Jet Acquisition Strategy and Timing

One of the least understood aspects of aircraft taxation is timing.

The same aircraft acquired by two different buyers can generate dramatically different outcomes depending on when and how the transaction occurs.

An effective private jet acquisition strategy evaluates:

- Fiscal year timing

- Corporate earnings projections

- Expected future income

- Regulatory developments

- Fleet planning objectives

- Exit strategy considerations

- Capital deployment priorities

The acquisition process should align with both operational and financial objectives.

When timing, structure, and utilization align effectively, aircraft ownership can become significantly more efficient from a tax perspective.

Aviation Asset Management and Long-Term Value Preservation

Tax savings are important.

However, sophisticated buyers recognize that depreciation alone does not create wealth.

True value emerges when tax planning integrates with professional aviation asset management.

Aircraft are complex assets affected by:

- Market cycles

- Maintenance history

- Engine program participation

- Cabin modernization

- Avionics upgrades

- Regulatory changes

- Fleet demand trends

An aircraft generating attractive tax deductions may still become a poor investment if resale value deteriorates unnecessarily.

The strongest ownership strategies combine:

- Intelligent acquisition

- Effective tax planning

- Professional asset management

- Strategic exit planning

This integrated approach often separates high-performing aviation portfolios from underperforming ones.

Cost Segregation Study Opportunities in Aviation

Many investors are familiar with the concept of a cost segregation study in commercial real estate.

Certain aviation-related assets and infrastructure investments may present similar opportunities for accelerated treatment of specific components, depending on jurisdiction and tax regulations.

These analyses can identify portions of an investment that qualify for alternative recovery periods.

While not applicable to every situation, advanced structuring techniques can sometimes unlock additional value beyond standard depreciation schedules.

Sophisticated buyers routinely investigate these opportunities during the due diligence phase rather than after acquisition.

Due Diligence Before Making Tax-Based Decisions

One of the biggest mistakes aircraft buyers make is purchasing an aircraft primarily for perceived tax advantages.

Tax benefits should support an acquisition.

They should never justify an unsuitable acquisition.

Before relying on projected depreciation benefits, buyers should evaluate:

- Business-use requirements

- Documentation standards

- Regulatory compliance obligations

- Financing implications

- Ownership structure design

- Future utilization forecasts

- Exit planning assumptions

The aircraft must make operational sense first.

Tax efficiency should enhance the transaction not drive it entirely.